Welcome to a/symmetric, our weekly newsletter. Each week, we bring you news and analysis on the global industrial contest, where production is power and competition is (often) asymmetric. To receive issues over email, subscribe here.

This week:

- High-tech dreams stand on low-tech beams. Or, industrial foundations matter.

- Weekly Links: Pragmatic AI. Why did the US miss the battery revolution? And the Uber-BYD deal.

Don’t forget the low-tech manufacturing

Grand visions of a high-tech future abound: roving fleets of robotaxis, buzzing swarms of low altitude drones, AI-powered factories turbocharging output, and a supercomputing internet, to name a few.

But let’s not forget: every single one of those high-tech dreams is dependent on low(er) tech inputs. Autonomous cars require steel. Drones use motors, plastics, and carbon fiber. Data centers use metal racks and copper grounding bars, and can’t function without air- or water-based cooling systems.

So, even as China pursues future industries, it knows that it must retain and strengthen its traditional industries — sectors like materials, machinery, electronics, minerals, and energy that, by one count, make up 80% of China’s manufacturing sector.

“Traditional industries are the foundation of the modern industrial system,” writes one Chinese academic in a recent Economics Daily essay. Far from representing the “low-end,” he adds, China’s traditional industries have “outstanding advantages in manufacturing level, industrial volume, industrial chain integrity, and international market share,” and should be fully leveraged for their comparative advantages.

Traditional vs. emerging industries: false dichotomy?

One of China’s most prominent proponents of traditional industries (also referred to as basic industries) is Lu Feng, professor of economics at Peking University.

In a 36,000 character essay published in March, Lu and his co-authors argue that a key reason for China’s slowing economic growth is Beijing’s misguided attempts to suppress the growth of the country’s industrial system.

Lu says the prime culprit is a decade-long government effort, beginning in 2013, to rein in overcapacity in traditional industries like steel, cement, aluminum, glass, and shipbuilding.

The effort was driven by what Lu describes as officials’ tendency to view the economy in two dichotomous halves: the old forces of traditional industries, which were to be de-prioritized; and the shiny new forces of high-tech and emerging industries, to be placed on a pedestal.

He draws on national statistics to make his case. From 2000 to 2012, China’s average year-on-year industry growth rate was 11.1%, higher than the average GDP growth rate of 10.1%. But in the decade since 2013, the pattern flipped: average industry growth rate was 5.7%, behind 6.1% for GDP.

The old-versus-new-industries mindset, Lu argues, is wrong. And it is rooted in the assumption that China’s development path must follow the “Western worldview,” he says — presumably a reference to the outsourcing of labor intensive, low margin activities to developing economies where costs are lower, and retaining only high margin segments of the supply chain.

#TradIndustries feedback loop

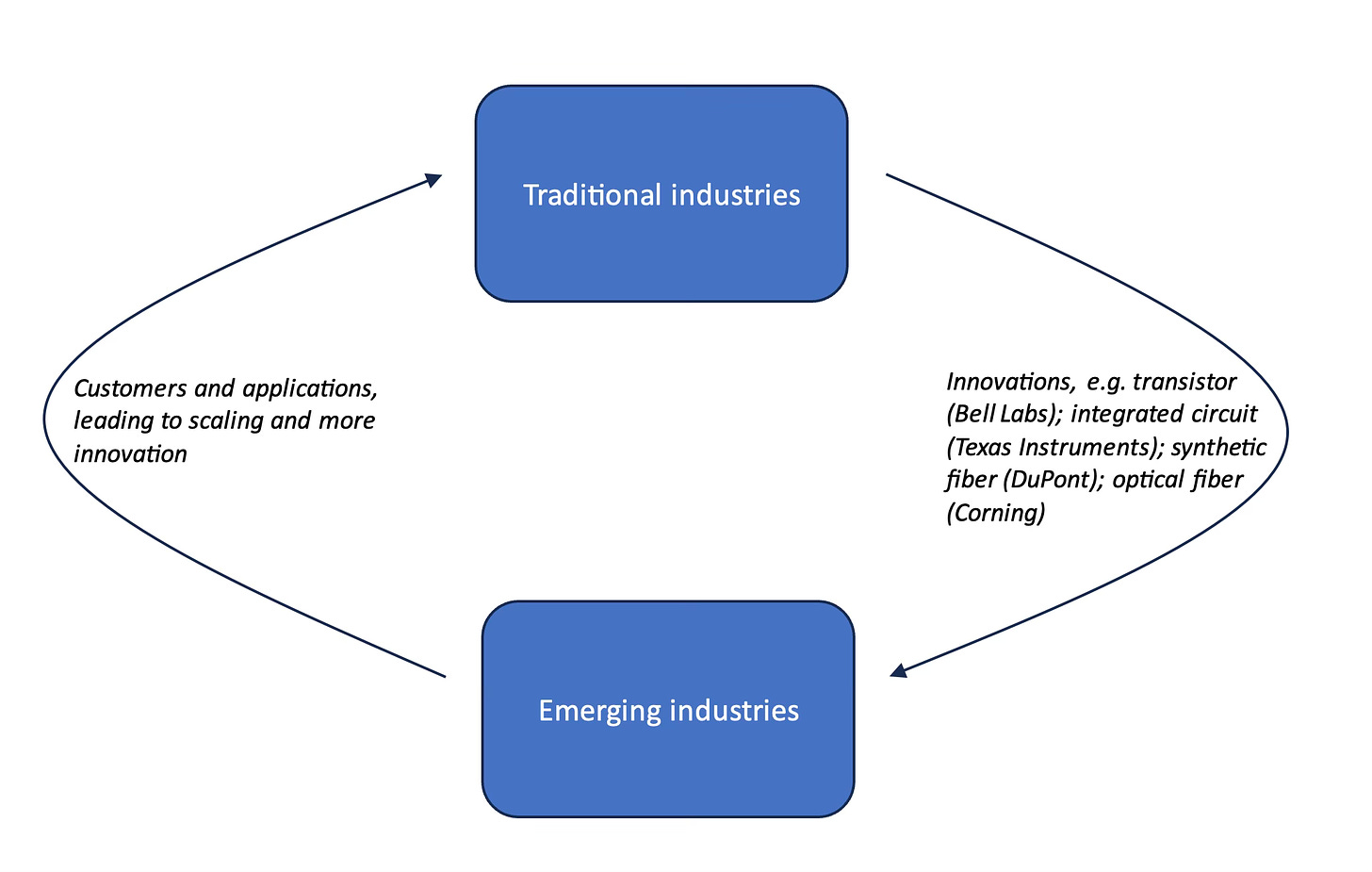

Perhaps it’s more helpful to think of low-tech, low-end industries as being in a symbiotic relationship with advanced, high-tech ones.

Consider the fact that traditional industries spawn emerging industries. Cutting-edge technologies don’t form in a vacuum, but are built on the accumulated experience and knowledge of existing sectors. History has shown this to be the case. Lu writes:

“The transistor was invented by AT&T’s Bell Labs; the integrated circuit was invented by Texas Instruments; the synthetic fiber was invented by DuPont, which originally produced explosives; the optical fiber was invented by Corning, which produced glass; and the prototype of the liquid crystal display was invented by RCA, but it was industrialized by Japanese consumer electronics companies. These inventions later developed into independent industries, namely the strategic emerging industries at the time, but they all originated from traditional industries.”

A sketch of a possible feedback loop between “low-tech” traditional industries and high-tech emerging ones.

Plus, “the main customers of the high-tech industry are still traditional industries,” Lu notes. One example might be 6G network equipment: listed as a future industry, but also used to upgrade a century-plus-old telecommunications industry. Another might be new materials like high-grade specialty steel, metal alloys, and engineering plastics: identified as a strategic emerging industry in 2010, but also squarely in the traditional bucket.

Emerging industries also find robust use cases in traditional sectors, which in turn provide space for the incipient technology to deploy, troubleshoot, scale, and commercialize.

Artificial intelligence is a case in point. As we have previously noted, while China may lag behind US leaders in developing large language models, it views industrial applications of AI as a way to gain an edge over foreign competitors. And leveraging industrial AI depends on having a sizeable industry to apply it to. Lu writes:

“…the possibility of applying AI to industry still depends on the application innovation of industrial enterprises (so the general LLM is not necessarily the optimal technical route of industrial AI)…Even if AI can have a significant impact on productivity improvement, it is still an ‘enabling’ technology, and cannot replace the existing industry.”

Frontiers and foundations

All this holds lessons for contestants in today’s global industrial competition.

In the US, there is broad recognition that the nation’s industrial base is insufficiently robust, particularly in relation to defense needs in both peacetime and wartime, but also across key sectors like public health and pharmaceuticals, clean energy, and logistics and transportation.

For its part, China is wising up to the indispensable role of its traditional industries. At last May’s meeting of the Central Financial and Economic Affairs Commission, Xi Jinping said China must “keep promoting the transformation and upgrading of traditional industries, and not take them as ‘low-end industries’ to be simply eliminated.”

Or, as Lu puts it: “Just as the United States has the hegemony of the US dollar and Russia has oil and gas, China’s industrial production capacity is its biggest strategic asset.”

Weekly Links

️ “Pragmatic AI.” Jen Zhu Scott of VC firm IN. Capital writes that tech and information constraints incentivize Chinese AI firms to use smaller LLMs, which may “lack the brute strength of their larger counterparts but they are cheaper to create and run.”

This pragmatism defines China’s tech ecosystem, where R&D is more focused on products that can be quickly commercialised, she writes. “This means that while the US ecosystem has the edge in groundbreaking innovations, China excels in execution: finding product-market fit, scale, and making applications highly affordable.” (FT)

️ Why did the US miss the battery revolution? A good overview of, and some hypotheses about, why the US managed to do “some of the key invention [of batteries], but more was done in Japan and the UK, and the key products were innovated and successfully commercialized in Japan.” The answer probably sits somewhere in the intersection of innovation, industrialization, industrial policy, trade policy, and the bare knuckle sport of global commerce. (Noahpinion)

️ BYD x Uber. A deal signed this week will offer drivers on the ride-hailing platform pricing and financing deals for the Chinese EV maker’s cars. The agreement will also see the two companies collaborating on “BYD autonomous-capable vehicles” for Uber’s platform. TP Huang’s take: “a very interesting deal and encouraging one for BYD’s global ambitions. It is also a major shot in the arm for BYD’s efforts in AI and ADAS.” (CNBC, TP’s Substack)

(Photo by: Karan Bhatia/Unsplash)