Welcome to a/symmetric, our weekly newsletter. Each week, we bring you news and analysis on the global industrial contest, where production is power and competition is (often) asymmetric.

This week:

- “Buy China” is no fan of “Buy America:” A brief look at Beijing’s toolkit of policies that favor domestic companies at the expense of foreign competitors.

- Weekly Links Round-Up: AI cooperation or competition? American businesses’ prospects in China. And Huawei’s resurgence.

“Buy China” vs. “Buy America”

China this week filed a complaint with the World Trade Organization against US tax credits for electric vehicles, allegingthat subsidies provided by the Inflation Reduction Act are “discriminatory, protectionist, and contrary to WTO rules…and are to be condemned.”

The irony of Beijing’s move was hard to miss. Observers deemed it “an act of colossal chutzpah,” “quite funny,” and “bold.” Afterall, China’s industrial playbook has long centered on spending vast sums to support its homegrown players while actively setting an uneven playing field to systemically disadvantage foreign competitors both at home and abroad.

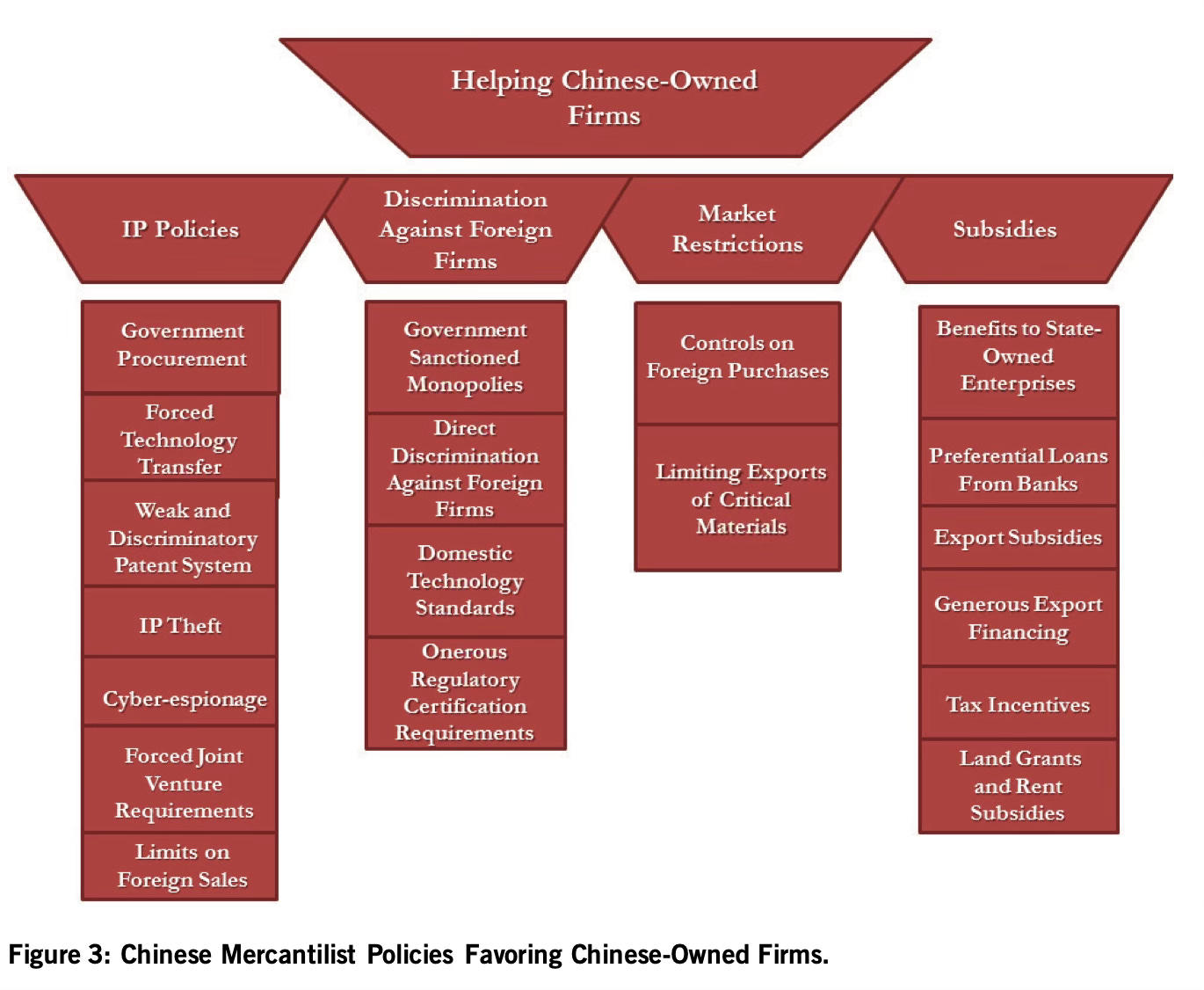

With Beijing protesting “Buy America” measures, let’s take a look at three hallmark “Buy China” policies.

Playing regulatory favorites

China uses regulatory hurdles to keep foreign players out, shielding emerging domestic industries from competition.

This happened with batteries. Beginning in 2015, only certified EV battery manufacturers were eligible for government subsidies. Of the several dozen battery makers on the whitelist, no major foreign company made the cut. Leading South Korean firms like LG Chem and Samsung feared getting shut out of the Chinese market.

Chinese state media, meanwhile, were saying the quiet part out loud: “Holding the policy ‘talisman,’ domestic EV battery makers reap dividends,” read an Economic Daily headline from 2016.

By the time Beijing scrapped its list of certified battery makers in 2019, domestic battery giants like CATL had already grown revenues and grabbed market share. People’s Daily said as much, reminding readers that no Japanese or South Korean battery giants had made the list, and that the whitelist policy had bought time for domestic battery makers to “improve and strengthen.”

Today, Chinese EV battery firms have over 63% of global market share—triple their share in 2015.

A special tax system

A carefully calibrated tax system helps China maintain its dominance over global rare earth value chains, essentially giving Chinese industry a built in 13% cost advantage over foreign competitors.

“…foreign magnet firms, which almost certainly rely on Chinese feedstocks of oxides, metals, and/or alloys, will produce magnets that are at least 13% more expensive than their Chinese counterparts.” — US Department of Commerce, February 2023

Here’s how it works.[1] The standard VAT rate is 13%; this applies to buying rare earth products in China (including oxides, metals, and magnets). A foreign buyer purchasing raw rare earth materials from China pays the international market price, including the 13% tax. When that buyer exports the rare earth materials from China (say, to a magnet factory overseas), the VAT isn’t refunded.

But here’s the catch: Chinese exports of rare earth magnets—which have more value added than raw rare earth materials—do get a VAT refund. That means Chinese rare earth magnets automatically enjoy a 13% raw material cost discount. This ensures China’s grip on the downstream segments of the rare earth industrial chain—from which it can exert leverage over the upstream.

A similar dynamic plays out in imports. A foreign miner selling minimally-processed rare earths to China doesn’t pay import duties. But more processed inputs like rare earth oxides and metals face a 5% import duty on top of the 13% VAT. This means foreign rare earth mining projects can only feasibly sell low value-added rare earth materials to China. Again, this helps maintain China’s dominance over rare earth processing and magnet-making.

Standards mismatch

Beijing has used domestic technical standards to disadvantage foreign players. And increasingly, it is using international standards to give its homegrown champions a significant leg-up in key industries worldwide.

A 2016 report by the Berlin-based think tank Merics put it this way:

“…China sometimes formulates national standards in strategic industries that deliberately differ from international standards in order to impede market access for foreign technology and to favour Chinese technology on the domestic market. Examples of Chinese national standards are the FDD-LTE standard for 4G mobile networks, the WAPI standard for wireless networks and independent standards for electric vehicle charging stations.”

As of 2019, foreign businesses operating in China still consider “requirements to comply with unique China standards and/or the inability to participate in the standard-setting process” to be a significant business barrier, according to a survey conducted by AmCham China.

Weekly Links Round-Up

️ Cooperate or compete? Emily de La Bruyère and Nathan Picarsic argue that AI engagement with China is a risky proposition. Precedent suggests that “Beijing will trade its purported cooperation on AI safety for relaxed restrictions on its access to cutting-edge US technology and US data,” they write. That assessment seems prescient: Chinese leader Xi Jinping has pressed Dutch prime minister Mark Rutte to rethink semiconductor export restrictions—in return for, among other things, greater cooperation in AI. (Force Distance Times, Politico)

️ US businesses are struggling in China. American CEOs this week made their pilgrimages to Beijing, and were urged by Xi to invest more in the country. But their prospects there are fast dimming amid greater local competition and sagging consumer spending. (WSJ)

️ Huawei’s resurgence. The heavily sanctioned tech giant said its profits doubled in 2023. And we reckon this is just the start of its upswing as the company pushes into autonomous driving, AI computing, satellites, and more. (CNBC, a/symmetric, China Space Monitor)

[1] This has been explained in detail by The Rare Earth Observer (see here) and Per Kalvig of the Center for Minerals & Materials, Geological Survey of Denmark and Greenland (see here, p.145)

(Photo by Sora Shimazaki))